Some thoughts on European Space in 2025

by Pierre Lionnet

The key global trends in 2025 were not the ones you think

Since 2019 every year is a new record in global space activity, and every year the previous record is slashed by SpaceX, with more launches, more satellites deployed, more mass to LEO.

Not only is this becoming repetitively boring, but it has now been 5 years that SpaceX has monopolised the global narrative in space. So I’ll put SpaceX on the side to focus on other things, the things that SpaceX’s impact on statistics tend to mask.

There are three non-SpaceX trends that are worth noting in a global context of growing space infrastructure deployment.

1. China’s is putting its money and efforts toward its ambitions:

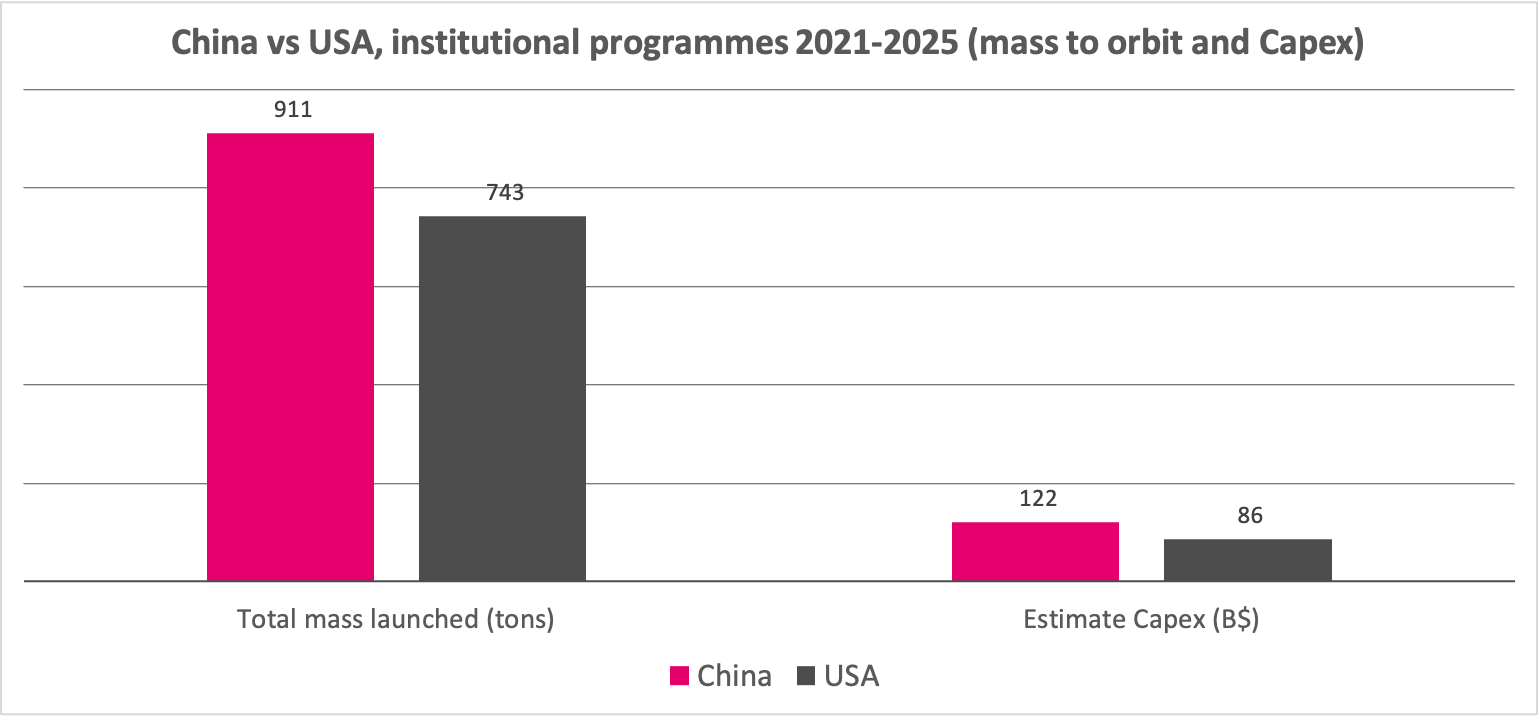

On all key metrics (spending, satellites, launch events and mass to orbit) the Chinese institutional space programme has surpassed its US counterpart over the past five years: we estimate that between 2021 and 2025 the Chinese space programme deployed 23% more mass equivalent to 40% more Capex to orbit than the USA[1].

The rise of China, which is pursuing all space domains at once, from military observation to planetary activities and human spaceflight, puts this relatively young space power at the forefront of space geopolitics, to the point that China has somehow become the nemesis of the US space administration who lives in fear that Chinese taikonauts may beat US ones with “boots on the Moon”.

2. LEO proliferation trends are transforming government space procurement.

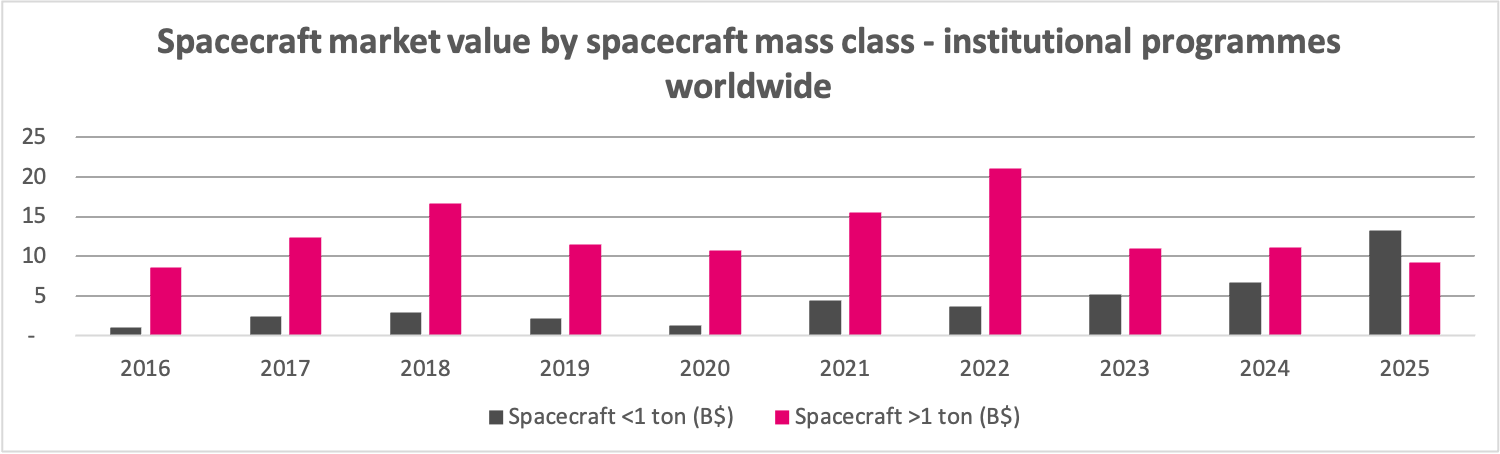

More, smaller, cheaper satellites produced in larger batches and series are becoming the new normal. As a result we have seen the average mass of institutional satellites divided by 3 to 5 in just two decades, with the share of small satellites (below 1 ton) now representing almost half of all institutional payloads launched, while they were less than a third two decades ago.

However, this is not about the smallsat revolution that was much talked about a decade ago, announcing widespread use of extra small satellites (below 10 kg). We now see that the ‘sweet spot’ in satellite production sits in a rather large bracket with the 80-150 kg class at the lower end (which include prominent players such as ICEYE), and the 500-1000kg class at the higher end (with Starshield by SpaceX, for example).

In 2025, for the first time, the market value of institutional satellites of less than 1 ton exceeded the value of the segment of larger satellites.

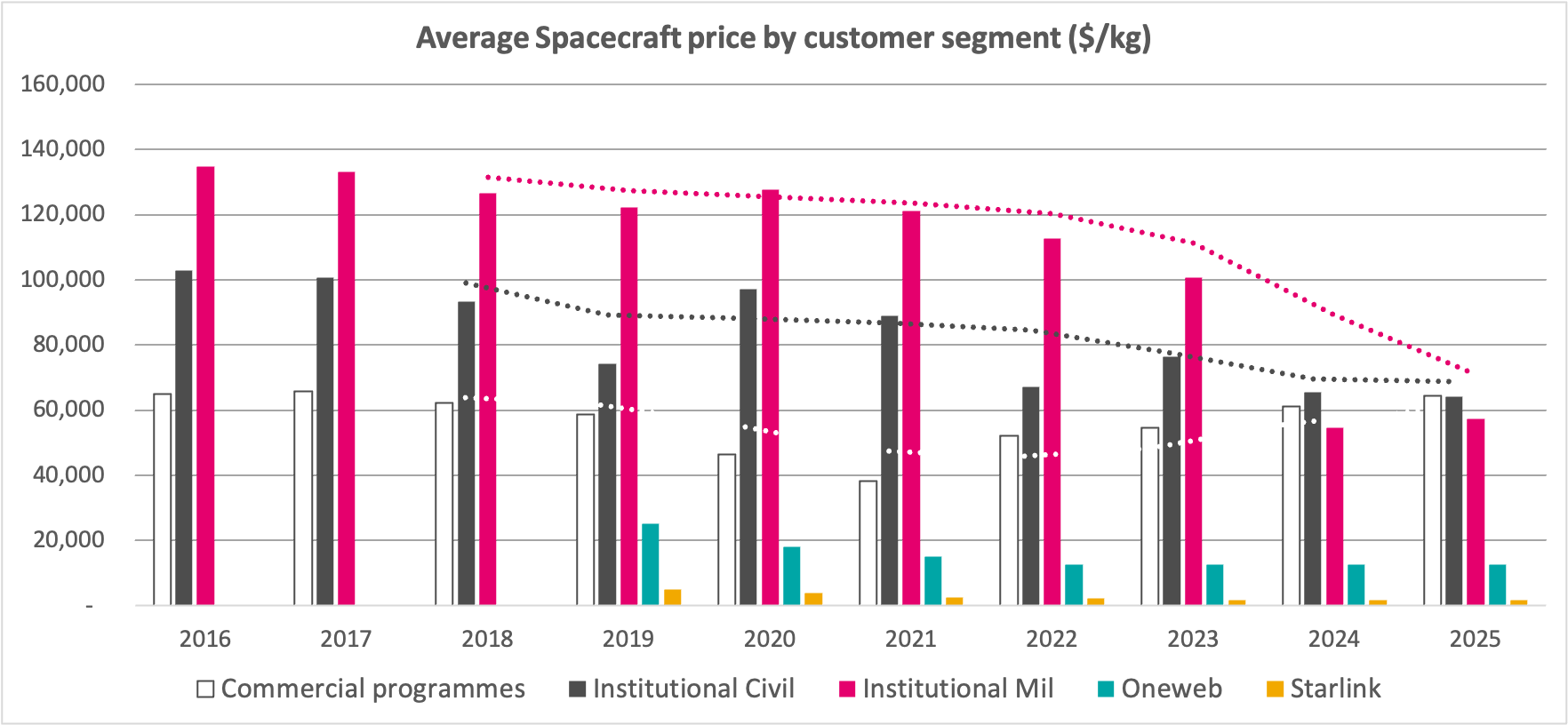

3. With more spacecraft produced in larger numbers, satellite prices are dropping, particularly in institutional programmes.

This is quite a unique phenomenon that was lurking already in 2024 and is confirmed in 2025: istitutional programmes’ price per unit of mass now aligns with historic prices of commercial spacecraft.

It is a consequence of the trend towards production in larger volumes and the relative standardisation of designs that was mentioned previously. Of course, there will always be exceptions, and very large, exquisite, expensive satellites, particularly for military and scientific programs (where values above 200-300k$/kg are not uncommon) will still be built, but the sheer impact in mass and volume of such low-priced programs such as Starshield and the PWSA in the USA or Yaogan and Shijian in China, have a major impact on global price averages.

It is worth noting still that these programmes are still much less affordable than their commercial counterparts like Oneweb (about 12k$/kg) or Starlink (about 1.5k$/kg), but overall the data confirms that producing in volumes can drive down the unit costs of space infrastructure, although this may imply to commit large budgets to create the critical mass of demand enabling lower acquisition unit prices.

This new industrial landscape doesn’t come without questions and doubts. Are companies bidding for these low-priced programmes able to sustain such low costs? Will the recurrent orders scaling the volume of demand allow a break even in the future? It is too early to tell, but the financials of key United States players partaking in the Proliferated Warfighting Space Architecture (PWSA) programme (York Space to cite one) may indicate that the economics of large scale spacecraft production are not solved by all. At least yet.

European accessible markets are receding

The redefinition of global spacecraft demand, and in particular the declining demand expressed by legacy satellite operators, particularly for geostationary ‘commercial’ satellites, has had a toll on the accessible market for European spacecraft and launch service providers. The accessible demand for European players on the commercial spacecraft segment has been almost cut in half in just a decade, with an average annual value of 2,5B$ in the past 5 years against about 4B$ a decade ago.

In contrast, the accessible demand for commercial launch services has been growing in recent years, thanks to the incremental demand spurred notably by the deployments of Oneweb and Amazon Leo (formerly Kuiper project). With about 2B$ in accessible launch demand (and growing) European launch service providers can look at the future with more optimism, although the competition with SpaceX (and new entrants) puts more pressure on prices. On both segments (commercial spacecraft and launch) Europe managed to capture a sizable share of the accessible demand (about 35% in average) except in launch, due to the unavailability of European launchers to serve the commercial market in 2024 and 2025.

Fortunately, European spacecraft and launch suppliers can still rely on a sizable volume of institutional demand which is typically considered captive. Of course, the European institutional demand is nowhere as large as its US and Chinese counterparts; it represented about 4-5B$ in the spacecraft segment but much less than 1B$ in launch in recent years. However, we anticipate further improvements on both fronts with European governments signaling their intention to further step up their investment in space programs.

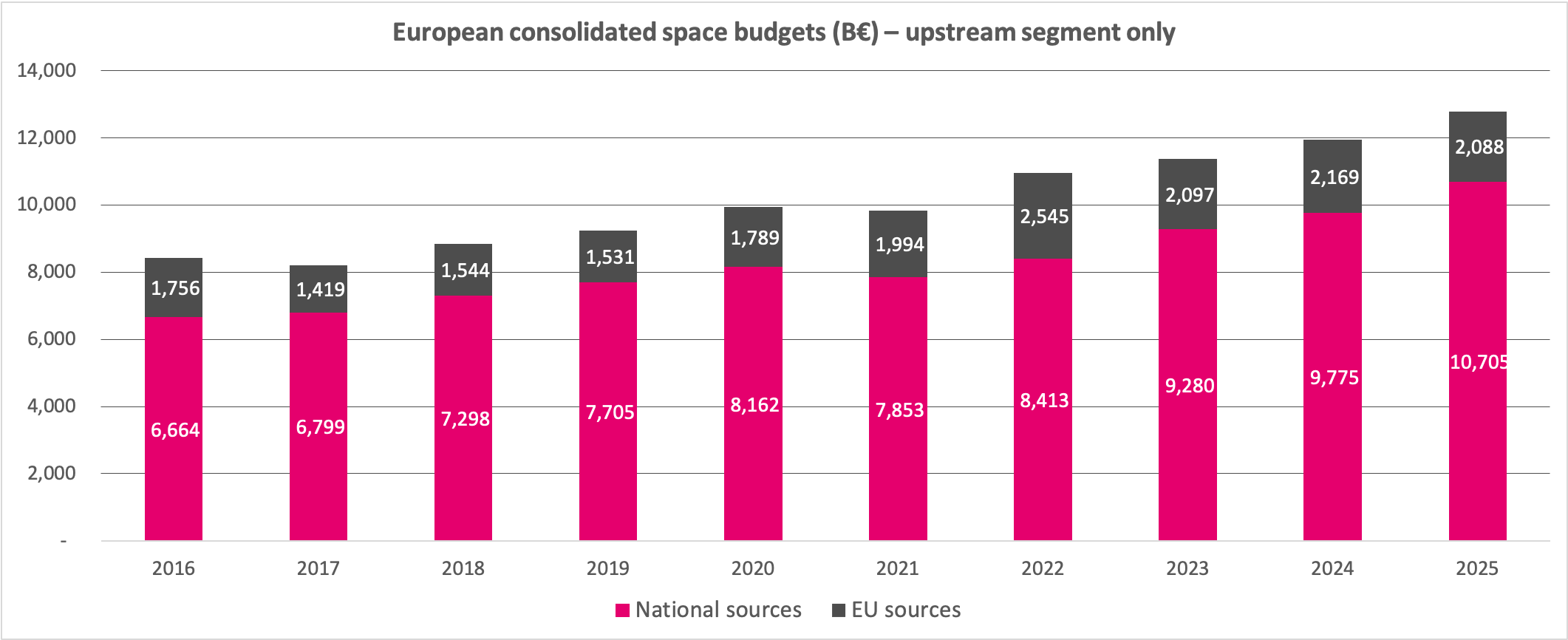

European space budgets

Eurospace keeps a tab on European governments spending on space programmes by consolidating budget data (to eliminate inter-agency spending) and by separating budget lines going to research institutes, downstream developments and large ground observatories. Over the years we have documented the growth of European space budgets peaking at almost 13B€ in 2025, i.e. 34% more than in 2016 (in current terms).

We anticipate this growth trend to be confirmed in 2026 and beyond thanks to the high level of commitments registered at the ESA Council at Ministerial level of October 2025, and following the growing interest of European militaries (with Germany at the forefront) in acquiring sovereign satellite infrastructure. The expected roll-out of the IRIS² procurement (totaling 10B€) should also drive higher budget commitments in the future.

The Slowing Effect of Georeturn

One particular feature of European space spending is that all national budgets (going to the funding of ESA, Eumetsat, and National space programmes) are driven by strong national return rules, whereas only the programmes like Copernicus and Galileo, funded through the European Commission, are (in theory) exempt from such stringent constraints.

Today a growing portion of European space budgets are driven by national return rules, up to 84% in 2025 (compared to 65% 5 years ago) with the consequence that increasing budgets at national levels are conducive to stimulating the creation of more production capabilities at national level, a situation that increases the fragmentation of the supply chain. This creates overall higher production costs and does not support the generation of significant economies of scale. And in fact we notice that as far as satellite costs are concerned, European institutional programs exhibit much higher costs per kg than in the USA (about 30% more in 2024 and 2025).

Looking ahead

ESA’s effective growth

“The largest contributions in the history of the European Space Agency, €22.3bn, have been approved at its Council meeting at Ministerial level in Bremen”.

The announcement was greeted with considerable enthusiasm across the European space sector, reflecting a steady upward trend in ESA funding: €14.5 billion in 2019, €16.9 billion in 2022, and now a record €22.3 billion.

Regrettably for the obsessive analyst that I am, comparing the outcomes of successive ESA Ministerial Councils is a constant source of frustration. The headline funding figure alone is not necessarily an indication of a genuine increase over the previous Ministerial, as ministers commit not only to new programmes but also reaffirm funding for existing ones, to varying degrees. As a result, the final total combines both new and previously committed funds, making year-to-year comparisons less straightforward than they first appear.

In short, a 30% growth of commitments does not linearly translate into the Members States spending 30% more every year through ESA in the next 3 years.

For example, our analysis of ESA's 2026 budget suggests that ESA's overall budget is projected to increase by 7.5% in 2026, including programme delegations from the European Union and EUMETSAT. However, the underlying increase in Member States' direct contributions amounts to “only” 10%, highlighting the distinction between ESA's total budget and national funding commitments.

Europe’s Military Rise

European nations have been living a cozy life under the protective umbrella of NATO, benefiting from the vast arsenal of U.S. military observation satellites. Only a few European nations have developed their own sovereign observation satellites, albeit with limited financial resources (especially when compared with massive U.S. military space spending). As a result, only a handful of European military observation satellites have been launched each year, with France, Germany and Spain leading the way.

With the Russia-Ukraine conflicts at its borders and the shifts in the Trump administration’s international agenda, making casual, and not so casual, hints that Europe may not be guaranteed the access to US satellites anymore, some European nations have decided to take the matter in their own hands.

Unsurprisingly, the geographical proximity with Ukraine has acted as a trigger, and as soon as Spring 2025 we have seen Poland, quickly followed by Germany, Finland, the Netherlands, Sweden and even Portugal, going on shopping spree to equip themselves with military-grade observation capabilities.

Interestingly, most of the orders went to ICEYE, the Finnish startup specializing in SAR satellite solutions. In just a few months, during the second half of 2025 and the beginning of 2026, ICEYE signed hundreds of millions of euros' worth of new orders, covering dozens of satellites, and announced plans to expand its production capabilities, including by establishing dedicated local production facilities and teaming up with local players in the countries where demand is strongest, particularly Germany (did I hear "national return"?).

The Bundeswehr wants it all

“The conflicts of the future will no longer be limited to the Earth’s surface or the deep sea. They will also be fought openly in orbit” said Boris Pistorius, German minister for Defence, in September 2025, and then he dropped the bomb, announcing that Germany will invest 35B€ in sovereign space capabilities by 2030.

A few weeks later Germany published its military space strategy, setting ambitious goals to deploy LEO constellations for observation and communications, and by the end of 2025 the 1.7B€ order for the SPOCK-1 constellation was finalized with a consortium bringing together Rheinmetall and ICEYE (did someone say “SAR”?).

By committing such a large spending in military space capabilities Germany is redesigning the European military space market structure as it creates the demand equivalent of a deep gravity well attracting small and large companies alike towards the massive opportunity.

As soon as January 2026 Germany had also doubled down with the Satcom BW-4 order - quickly dubbed by observers “the German Starlink” - a project maybe worth 10B€ involving hundreds of satellites for which OHB, Airbus and (again) Rheinmetall seem to be joining forces.

Of course, the coexistence of the German-led Satcom BW-4 and the EU-led IRIS² project, which share a lot of stated objectives, raises many political questions, but from the supplier industry perspective it is mainly a question of aligning the production capabilities to satisfy the surge in demand, including the guarantee that the Bundeswehr satellites will be built in Germany (and, if possible, launched by a German launcher?).

France bets on Oneweb

France is also signaling, although with less panache, its ambitions to secure more sovereign space capabilities, as it decided to up its share in Eutelsat from 13 to 30% with a 1.35B€ investment in June 2025. Eutelsat, the owner of the Oneweb constellation, was instantly upgraded to the status of French “nugget”. Oneweb, originally a purely commercial endeavour, may now refocus towards the provision of services to the military, starting with the recent CENTAURE contract to provide LEO services to the French army.

France has also secured the production of the next generation of Oneweb satellites in Toulouse, where Airbus has conveniently repatriated from Florida the satellite production facilities. With the operator and the supply chain now secure within French borders, Oneweb increasingly looks like a French sovereign programme.

Spain re-order Spainsat NG II

In October 2025, Hisdesat (Spain’s military satellite operator) launched its latest GEO bird, a large programme worth 2B€ all included to provide secure communications. Unfortunately, the satellite was hit by a high-energy particle and was declared completely lost a few months later. Luckly, the satellite was insured, and Spanish authorities quickly moved to ordering an exact replacement, signaling that GEO solutions still have a role to play in military communications.

Bromo: It had been brewing for a year

Project Bromo, the “MBDA of satellites in Europe” as it is sometimes referred to, was announced at the Paris Air Show in Le Bourget in June 2025. The project aims at consolidating into a single organisation the satellite activities of the three key players in European satellite development and manufacturing: Airbus, Leonardo and Thales. It took a few more months and the companies signed an MoU in October that officially launched the work towards the creation of a new company jointly owned by Airbus (35%), Leonardo and Thales (32,5% each) by 2027.

Bromo would achieve a high level of concentration of the European satellite supply chain, with the three entities involved representing about 37% of the total space industrial workforce in Europe, with the promise of increased efficiency and enhanced competitiveness to address shifting trends and priorities in the global commercial and institutional satellite markets.

In a rather sobering way, Bromo was announced in the wake of concerning profit warnings affecting the space businesses of the BROMO partners. While low or negative profits have been affecting many in the European space sector for a while already[2], Bromo comes as a wake-up call for Europe: losing money on space business is not an option, and the industrial model needs a shake-up.

It is a little concerning, though, to see that the creation of a supranational giant in satellites may be missing on the opportunity of tapping into the vast potential of a growing European military demand, where local players (such as OHB and Rheinmetall in Germany) may have more appeal to national authorities with national sovereignty as a beacon.

On the other hand, Bromo may become the go-to solution for all EU programs where national return is not a requirement, even as its size is likely to prompt a broader EU discussion about how to balance industrial ambition with competition fairness. Of course, Bromo will be a key contender in the global commercial satellite market, and while size alone is no per se a guarantee in a consolidating sector, the three companies behind the project are betting that a player of Bromo’s stature could well tip the scales in favor of the recovery of a market that might otherwise continue to shrink.

European launchers are back in the game

After two years of reduced activity, European launchers have stepped up their game in 2025, with 7 successful launches in the year (3 VEGA and 4 Ariane 6) with immediate and positive impacts on the European launcher supply chain in terms of revenue and profitability improvement [3].

The demand for European launcher is definitely looking up, with Ariane 6 well positioned to deploy an increasing number of Amazon satellites, and the demand for VEGA being laced with Italian national programs such as the IRIDE constellation or the Platino SAR (did I say SAR again?) satellite series. Both launchers have a privileged access to the European institutional launch demand, which, as we have seen previously, is slated to grow.

2025 should also have been the year where we would have witnessed new European launchers succeed their maiden launches. Two leading German startups, Isar Aerospace and Rocket Factory Augsburg (RFA), created a lot of expectations, but none qualified in 2025. On top of this Orbex, the UK contender in the ESA’s European Launcher Challenge (ELC) programme, eventually folded at the end of the year lacking the capital resources to complete development.

"Space is hard" they say, but with the ELC ESA is supporting the development of a new breed of small launchers, Isar and RFA are still in the race, together with France's Maiaspace and Spain's PLD. A flurry of national initiatives are also supporting the same ambitions.

Nothing about European startups?

I could mention the sad passing of a few European startups (no, Orbex was not the only one) but better focus instead on the good news. Access to capital for European startups was sustained in 2025 with the largest equity raises concentrated in just a few companies, mostly with a focus on satellite series production (Endurosat, ICEYE, Aerospacelab and Sateliot undertook the largest capital raises, with more than 400M€ overall in 2025). The equity spree is stronger in 2026, and at mid-year we have tracked more capital invested in European startups than for the full 2025, with a similar focus on satellite capabilities (notably ICEYE raising 450M€ more).

Forecasting for 2026

2026 is already showing all the symptoms of being a good year for the European space industry with growing opportunities in institutional programs, and growth prospects in this segment on the medium term with the visible uptake of institutional spending, but the decreasing trend in GEO orders is confirmed. Legacy players are increasingly moving to smaller birds (mostly for national operators), or reorganising their fleets in a wave of mergers and consolidations, even resulting in the cancellation of previous orders[4].

The global, and European, space infrastructure industry is now facing a big reset. After proving that you could launch a broadband access LEO service and not go bankrupt by completely redesigning the industrial engineering of launch and satellite manufacturing, SpaceX is now looking at the next frontier application in space: the orbital compute. Another space engineering revolution seems to lie ahead of the sector, and all actors are rushing in to propose their own version of it. In the meanwhile a quieter transformation is happening in public procurements, with military programs embracing the LEO proliferation trend consistently within all space faring nations. The questions of overpopulation in LEO will become more pregnant and while this creates a ‘market opportunity’ for space surveillance tracking and orbital management services, it may also reveal earlier than expected the actual limits of growth in LEO applications.

[1] These are the Eurospace estimates of the value of space infrastructure deployed to orbit including launch service, based on purchasing power equivalents (a feature of Eurospace LEAT economic model). This is not an estimate of the total budget spent on government space programmes in the USA and China, in particular it doesn’t include the potentially very large spending going to contract R&D, mission concepts, ground infrastructures, agency staff salaries etc.

[2] https://www.thespacerepublic.news/p/where-are-the-profits-of-the-space

[3] It is worth noting, though, that the long delayed maiden launch of Ariane 6, unable to timely fill the shoes of a retiring Ariane 5, and VEGA-C’s Zefiro’s trouble (that caused the loss of two Pleiades Neo satellite with mission V22) have left Europe without an independent access to space for the most of 2023 and 2024.

[4] https://spacenews.com/ses-joins-eutelsat-in-canceling-geo-expansion-satellites/

Pierre Lionnet is an economist with more than 30 years of experience in the space sector. He is a well-known expert of space markets and technology trends and the Research and Managing Director of Eurospace, the leading trade association of the European space industry.

All data and figures presented in this article are © ASD-Eurospace. For further information or to request reproduction rights, please contact Pierre Lionnet at pierre.lionnet@eurospace.org.