Where are the profits of the space industry?

Pierre Lionnet

It all started in April 2024 when one of the biggest of Eurospace members, Airbus Defence and Space, was about to release its first profit warning on their space systems business. Airbus was about to register a 900M€ loss on its 2023 space revenues, an amount so large (worth 11% of the whole European space sector’s final sales) that it raised serious concerns on the overall sustainability of the industry. If Airbus was struggling, who wasn’t?

To find out, Eurospace launched first an examination of its member companies, asking them to complete an ad hoc survey disclosing the actual profits they registered on space activities, then the survey was enlarged focusing on European pure space players with published annual accounts.

Eventually Eurospace built up a representative sample of European space companies composed of 61 companies representing about 70% of the total European space business, for which we collected two very basic indicators: the total space systems sales, and the resulting EBIT (Earnings Before Interest and Taxes) for 5 consecutive years (2019 to 2023). We also collected data for 2024, but due to the low process of publishing and formally filing accounts, the 2024 body of data is not as complete and thus less representative than the other years.

Winners and Losers

The European space sector is highly concentrated with 4 large players (Airbus, Thales, Safran and Leonardo) controlling close to 60% of total industrial capabilities. Airbus D&S is the largest of them all (worth 18% of total European space workforce). As a consequence when Airbus posts unusually large losses on space systems, there is a high chance that this will affect the whole sector economics, and indeed we found that the total losses posted by Airbus were large enough to heavily tilt the scale towards negative profit indicators for the sector as a whole. But that is not the whole story.

The reality of the day is that the European space sector is facing increasing challenges

What we found is that in Europe space systems development and manufacturing is hardly a profitable business for the majority of companies in the sector, and for the rare instances where the bottom line is positive, the profits are clearly following a decreasing trend.

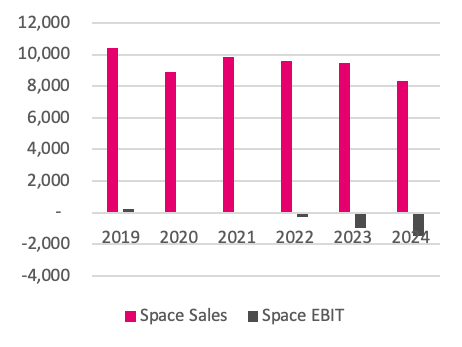

The chart below provides an overview of the annual space sales and related total profit made on the space segment (measured by EBIT: Earnings Before Interests and taxes) for the companies in the sample. In 2024, the sample losses (in gray) were worth 1,5B€ for a total space sales (in red) of 8,3B€.

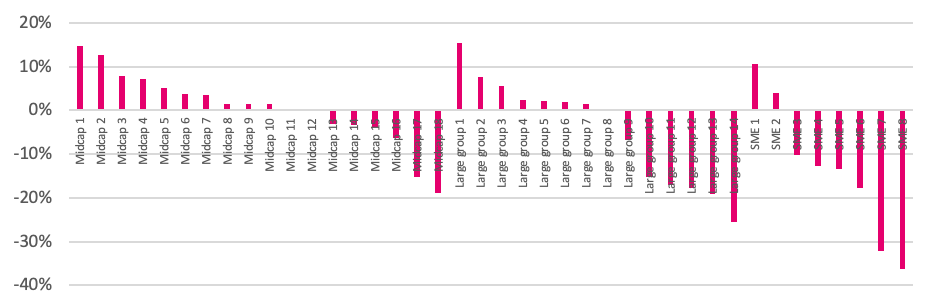

In 2023 we found that out of the 61 companies in the dataset, only 19 had a positive bottom line[1]. Even when setting aside the 21 startups of our dataset, whose abysmal level of losses makes their rendering into a chart very complicated, we find that on average, segment by segment, the situation doesn’t look good. In fact, when compiling the unweighted[2] profit rate of all companies (but start-ups) we registered an overall 4,6% average loss for the 40 companies in our sample. Even for the companies with a positive outturn in 2023 (see figure 2), the profit rates were not very high with only 4 companies in the sample posting profits above 10%. Net losses above 10% are, in contrast, very frequent, affecting 13 other companies in the sample (and the 21 start-ups too).

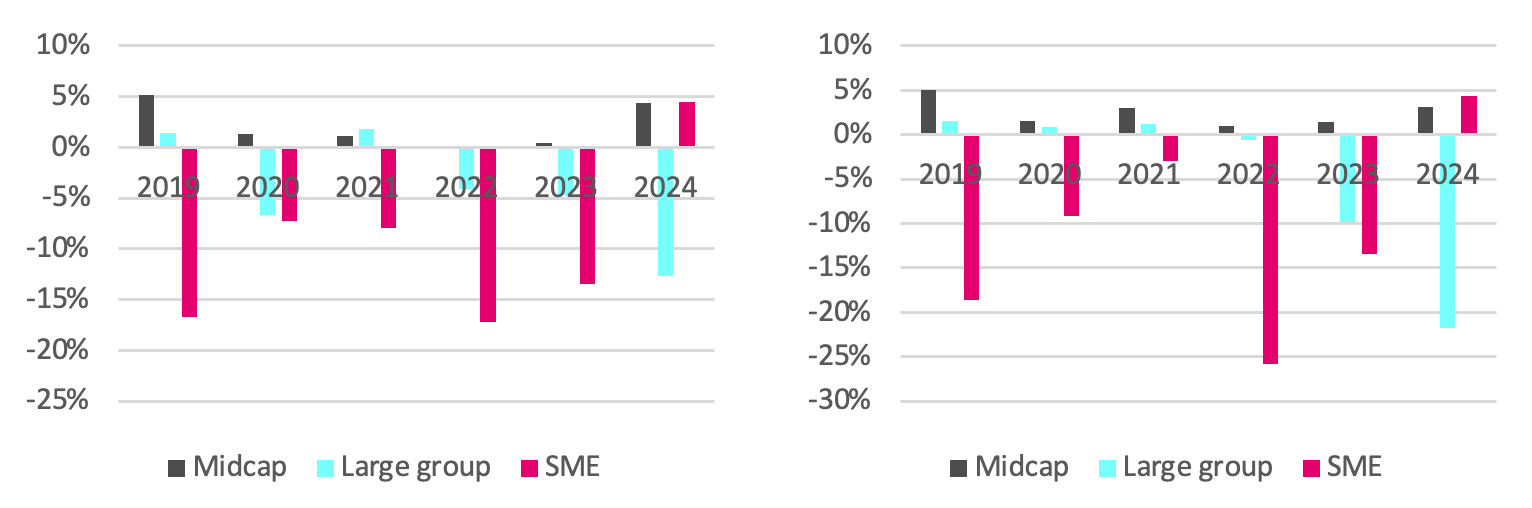

The situation is globally more difficult for Large groups[4] (avg. unweighted loss of -4,6%) and SMEs (avg. unweighted loss of -1,3%) than for Midcaps (avg. unweighted profit of +0,4%).

For the majority of start-ups in the dataset, the financial information shows extreme variations, with the majority of companies being pre-revenue and thus registering very high losses every year. Moreover only a handful exhibit sizeable revenues.

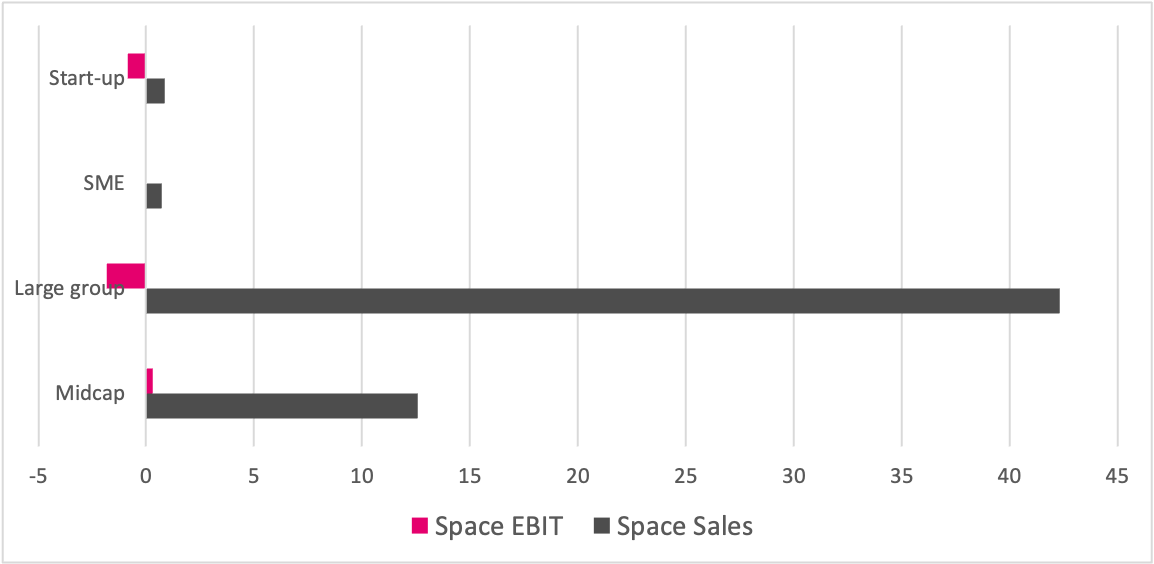

In aggregate, meaning all the companies included in the survey over the past 6 years, the sector recorded a total net loss of €2.4 billion on €56 billion in sales (–4.3%) (see Fig. 3). Excluding start-ups, the result improves slightly, with total losses of €1.5 billion (–2.7%).

When looking at profit rates in the sample, we notice a clearly receding trend, affecting Large Groups, Midcaps and SMEs.

The first striking point is that within all groups, and for all years, the profit rates have been very small at best and strongly negative at worst. The situation of SMEs in the sample is particularly concerning, with negative profits being the rule, and not the exception. Start-ups are not even pictured due to their profit rates being in the higher two to three digit negatives. We also notice that in all groups the situation is not getting any better with time (Fig. 4). The Midcap group in particular sees its profit rate receding (except in 2024, but the reference data is less representative[5]). It cannot be overstated that such a situation is not viable in the long term.

The Cost of Unsustainable Business

The reality of the day is that the European space sector is facing increasing challenges with the growing pressure on prices applied by its historic customers on one hand, and the growing competitive pressure on the supply side on the other hand, as many newcomers have entered the market in recent years (to the point that employment is growing at a much faster pace than sector revenues).

The sector is also experiencing the dramatic transformations affecting the commercial side of the business, and in particular the receding demand for large geostationary satellites, where the European space industry enjoyed comfortable market shares in both satellite and launch. The results are lower profit margins and unsustainable economic conditions for most of the European space industrial sector.

Within all groups, and for all years, the profit rates have been very small at best and strongly negative at worst.

When looking back in time for just the largest players in Europe we find profit rates navigating between 3% and 7% in the years 2014-2018. A previous survey performed by Eurospace with its members in 2002 revealed that individual profit rates were usually between 2 and 6%, with an average sector rate of 3,6%.

Looking at the wider Aerospace sector, a survey carried out by ASD in 2005 revealed that operating margins (that are usually higher than EBIT, or real profit) in the aerospace sector between 1985 and 2004 were rarely above 6% and averaged at 3,6%.

The association of European Space SMEs published the results of their own survey revealing that for SMEs active in European space programmes the return on investment is generally receding, from an average slightly above 4% in 2015 down to 3% in 2023, and for most of these companies space systems are only a small share of their total business.

The European space industry clearly suffers from a global profitability problem, with consequences potentially spreading throughout the whole sector, especially because when the large prime contractors suffer a profit crunch they may increase the pressure on their suppliers, with cascading consequences in the supply chain. Low and negative profits also mean that the customers are not paying the full value of the products they are buying, but while this can enhance the perceived competitiveness of the sector it is not viable in the medium to long term.

When looking at the situation across the Atlantic, and putting things in a longer term perspective, we find that going back to 2014 the larger US players in the segment have experienced globally receding profits, dropping from a hefty 12-13% in the years 2014-2015 down to 8% in 2021 and posting globally negative profits (-4%) on space systems as early as 2022. Here again the situation of one key player (Boeing) deeply affects the whole, but still.

The segment reporting for major players has progressively removed the details that would enable to identify the profit dynamics specific to the space segment, so we are now left to conjectures were it not for the financials of a few small space pure players trading on NASDAQ (of the infamous space SPAC wave of 2020-2021). For this group the situation is bleak. Even the best in the group like Rocket Lab have yet to close a profitable exercise after 19 years in operations, and have accumulated close to 1B$ in losses despite annual revenues in excess of 400M$ in 2024 (and growing). The others (such as Terran Orbital, AST Space Mobile, Planet, Momentus etc…) are not faring any better as shown by their detailed financial statements, not mentioning those that were delisted or went belly up (Astra, Virgin Orbit e.g.).

We are regularly served with an extremely optimist narrative that the space economy is growing (faster than the rest of the economy) and that the space business is huge (with hundreds or thousands of billions in revenues), fueled by the ‘fat profits’ enabled by the lavish spending of governments’ space programmes soon to be topped with the massive opportunities offered by new commercial applications. However, this is not verified by observable facts. Space is hard, they say, and making a profit in this sector is probably even harder, particularly within the critical segments of space systems manufacturing and launch.

[1] These 19 companies posted 170M€ in profits out of 3B€ in sales (5,6% profit rate), while the rest of the sector suffered from 1,1B€ in losses.

[2] Profit rate for the sector can be unweighted, i.e. the simple average of each company’s profit rate, irrespective of each company size, or weighted, where companies with larger sales proportionally weight more than smaller companies.

[3] Start-ups not included for chart readability. Of the 21 start-ups included in the dataset, only 4 have positive EBIT, while the majority in the lot has losses exceeding two or 3 digit percentage of sales.

[4] Within a single group the profit situation can be very different depending on the subsidiary considered, with some posting profits and other suffering losses, resulting in low or negative profits at group level.

[5] The data for 2024 is not as representative as with previous years, in particular in the Midcap and Newspace groups we note that the relative size of the sample is much smaller: about 60% for Midcaps and 40% for Startups. The 2024 indicators for these groups may not be comparable to the ones of previous years.

Pierre Lionnet is an economist with more than 30 years of experience in the space sector. He is a well-known expert of space markets and technology trends. He is the Research and Managing Director of Eurospace, the leading trade association of the European space industry.