Who are the most successful European startups?

Pierre Lionnet

Who are the most successful European space start-ups? And how do we measure that success in quantitative terms?

With about 1B$ raised in equity, the year 2025 confirms that there is still private equity appetite for European space ventures, even though the European “newspace” environment remains structurally much less conducive to raising equity than its US counterpart that clocked in at over 9B$ the same year.

The US fundraiser context in 2025 was marked by a few mega rounds (>500M$) mostly focusing on the domain of launch with Relativity, Rocket Lab, Firefly and Stoke Space leading the game, but the European startup scene confirmed in 2025 its capacity to attract large funding rounds (>100M$), as it already did in 2024 with a more diversified range of activity than in the US. In Europe the bias towards launcher development is not as strong as in the USA, and the investing environment is more balanced and leans more towards the building up of satellite and constellation capabilities.

All together, Eurospace estimates that European new space start-ups [1] have created more than 16000 new jobs in the European space sector in the past decade, while raising a total of 11B$ in equity [2].

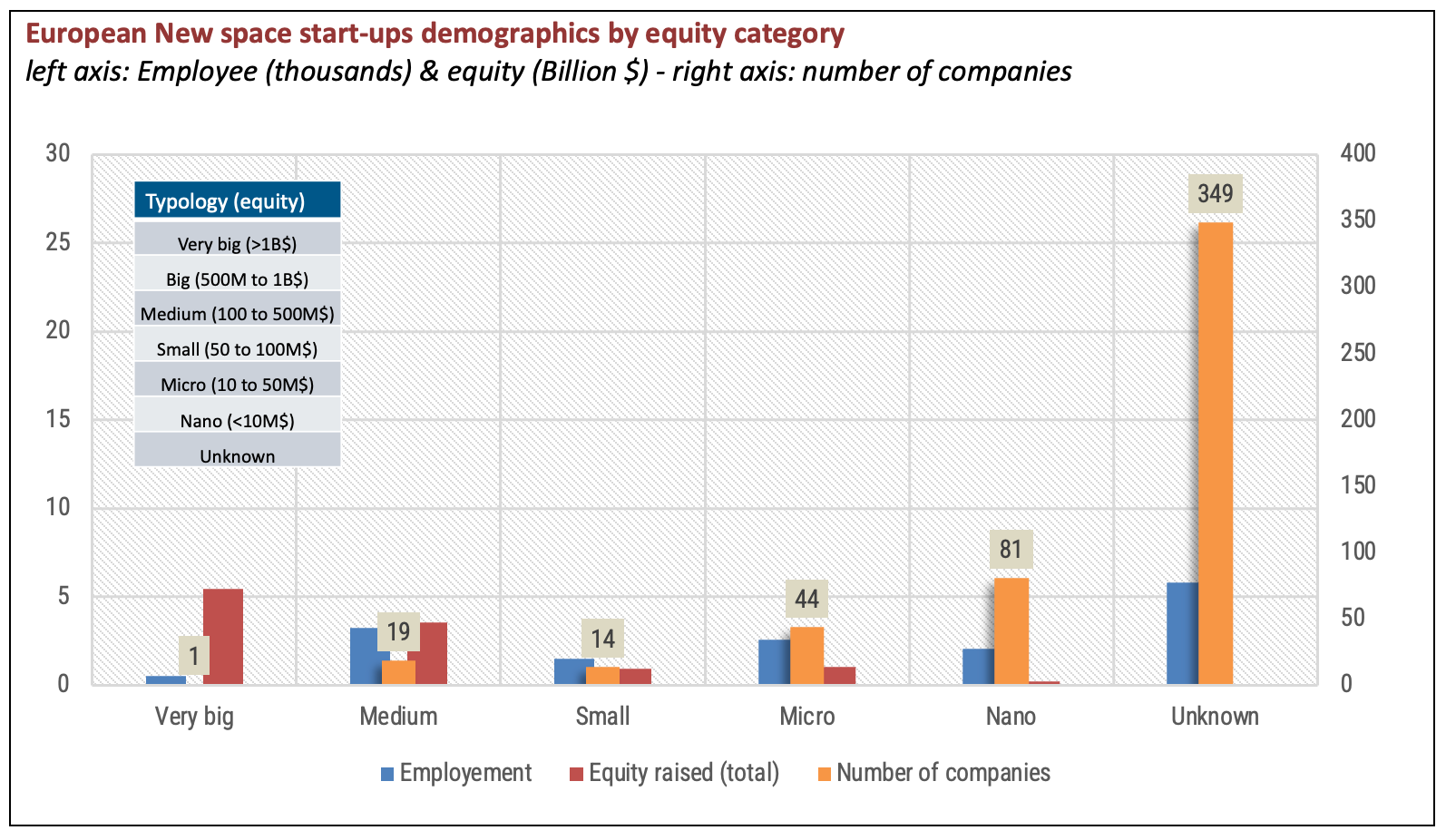

While the startup segment in Europe is composed by a majority of microscopic businesses, with 500 companies having total employment of less than 30 employees, the European space start-up scene has also proven its capacity to bring into the industrial landscape new actors able to reach a critical mass of capital and workforce, with some of them already boasting operational systems and capabilities.

So, who are the most successful European space start-ups? And how do we measure that success in quantitative terms? Let me share here my (hopefully as objective as possible) roster of the most relevant and significant players based on size and capabilities.

The most significant players on the European scene

Today’s most immediate measure of success for any start-up is the total equity raised. In Europe, differently than in the US, space start-ups have yet to achieve unicorn status (i.e. raising more than 1 billion in equity), with the notable exception of Oneweb that raised close to 6B$ in equity over its somewhat troubled life until its acquisition by Eutelsat.

But equity cannot be the sole measure of success, we also need to assess the level of operational success, and the development of industrial capabilities to deliver systems and services to customers.

Equity-wise Europe showcases less than 20 largish players that raised more than 100 M$ in equity, with the largest closing in towards 600M$ in capital raised. This small group collectively grabbed almost 4B$ in equity over the decade and has created employment opportunities for more than 3300 European workers. They are today’s driving force behind the European newspace.

One common feature of these top players in the European newspace is that they have invested market segments that were not pursued by large legacy companies.

They are led by best-in-class SAR constellation operator from Finland ICEYE, which has recently made headlines in Europe for both massive fundraising activity in 2025 (closing one of the largest equity rounds in the European space) and a flurry of government contracts to provide a mix of satellites and intelligence services to military forces in Europe and abroad.

ICEYE brings a unique combination of operational capabilities with close to 50 satellites launched since 2021, a growing workforce exceeding 800, and established industrial ventures spanning out of Finland to Poland and Germany. The Finnish outlier has demonstrated that you could grow a serious industrial capability at scale starting from literally nothing in less than a decade.

The runner-up position is slightly more difficult to determine, but with the variety of metrics involved, the best candidate is probably D-Orbit, that brings under the same roof a growing array of capabilities, a steady state of realisation with more than 70 payloads delivered through their “last mile” orbital service, and 20 ION spacecraft successfully deployed in just 5 years.

The company that originally positioned itself as an in-space logistics solutions provider has raised more than 200M$ in equity, has a workforce in excess of 400 and operations in Italy and the UK. With the recent acquisition of Planetek, D-Orbit is unfolding a new strategy towards the downstream, to accelerate its power play in the European space.

To complete the podium, among many possible contenders [3] (such as historic/mature cubesat players like AAC Clyde, ISISpace or Nanoavionics) I believe the third position has to be shared between two similarly sized players, both with flight proven expertise and both venturing towards the USA, while entrenching their core capabilities in Europe: the Belgian Aerospacelab and Bulgaria’s own Endurosat.

Aerospacelab is building from scratch an industrial capability to compete with established actors in Europe, with a small-satellite factory boasting the capacity to integrate small to medium size satellites in series up to a few hundred satellites per year. The company garnered the second largest fundraiser round of 2025 (110M$, for total equity now in excess of 160M$), has deployed 8 of its own demonstrators mostly in the in the 100-200 kg class, and is about to go live in 2026 with its brand-new integration plant.

With about 300 employees, Aerospacelab is no longer an SME, and is no more the large fish in a small pond: the company was pre-selected by the SpaceRise consortium for the LEO component of EU’s IRIS2 programme, where it competes with Airbus.

Endurosat is the Bulgarian lightweight contender who has recently been punching way above its class by securing the largest equity rounds of 2025 (for a total 165M$) in Europe. This large capital influx propels the company on a positive growth path and gives Bulgaria a unique space capability, while the country is not yet an ESA member state (despite being a PECS signatory for more than a decade now).

With nearly 20 satellites launched since 2021 (mostly cubesats in the 20 kg class) and more than 250 employees, the company was able to be selected as a potential vendor by no less than the US Missile Defence Agency within the SHIELD (Scalable Homeland Innovative Enterprise Layered Defense) programme.

In the top pool of heavily funded new space startups we also find a few very well-known players that have yet to reach operational capabilities, whether they are developing small launch systems, in the guise of ISAR, RFA, Orbex, and Maiaspace, or developing the building blocks of LEO human orbital infrastructure like The Exploration Company. With equity levels ranging from 150 to 460M$, and employment levels that often exceed the 250 mark, these companies are progressively outgrowing the SME status and are moving fast towards becoming prominent midcaps players in the European industrial landscape. All of them are now participating to major ESA or national space programmes, with varying levels of involvement, and are accelerating their path towards achieving a minimum viable product and start delivering operational systems and services to their customers.

Small launcher companies are on the hottest seat, with many maiden launches announced for 2026, starting with the next ISAR Spectrum launch as soon as March.

Unlocking demand

Unlocking actual demand is probably the most difficult step to grow for European newspace players.

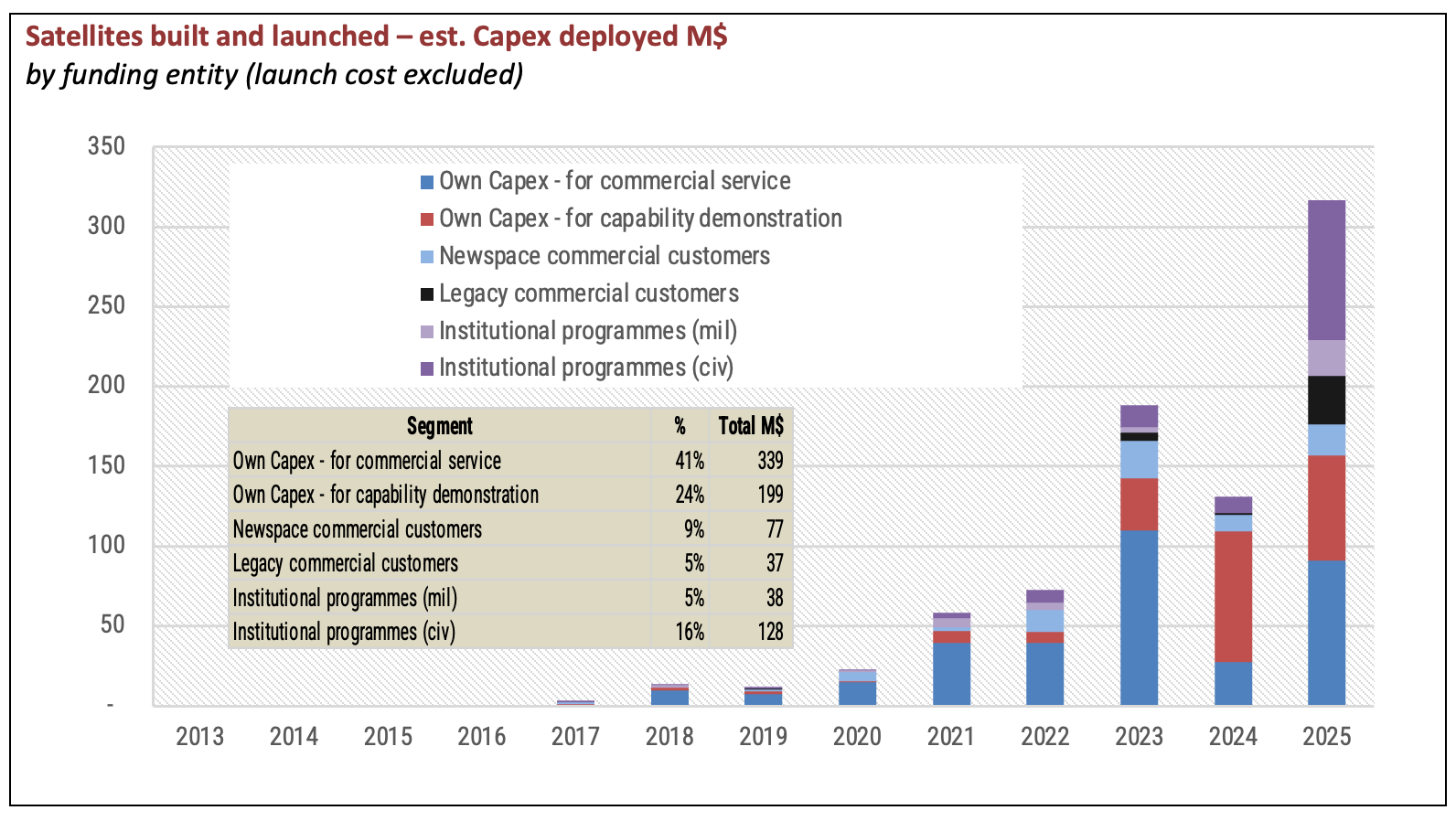

Eurospace’s analysis of actual spacecraft deployed by European space start-ups shows that they deployed about 800M$ worth of satellites by the end of 2025, with half of that capacity to provide operational services to their customers funded out of their own resources. Players seeking revenues selling spacecraft to third party customers have found some level of success, particularly with European institutional programmes that procured almost 180M$ worth of spacecraft according to our estimates.

A lot of companies’ Capex (about 200M$) was directed towards funding demonstration missions to gain credibility with potential investors and customers. Aerospacelab has been particularly prominent in this area, with 8 self-funded demonstration missions so far.

Of course, the road to success and durability is still a rocky one to trod. And there have already been losses on the way. Mynaric, once among the most promising European space startups, trading on NASDAQ (USA) and FRA (DE), entered a “restructuring plan” in 2025 and was de-listed, seeking a way out of debt, with dire consequences on the original shareholders. Orbex had to close its Danish subsidiary the same year, citing heavy losses and negative equity as the root cause, while the UK mothership is seeking to be recapitalised through its acquisition by The Exploration Company as announced in January 2026.

Other players have also folded in the past, such as Astrocast, Swiss Space Systems, SpaceAble, Spark Orbital, or Kleos Space to name a few. The fate of some very prominent actors, like Rivada Space that claimed billions in funding from unnamed backers, is very uncertain.

The way ahead

For the survivors the way ahead is still full of headwinds and obstacles, starting with the struggle to secure customer revenue and achieve profitability of operations. The recent Eurospace profit survey, relying on open-source filings of accounts of a growing set of European space start-ups (25 start-ups are included), shows similar trends for these companies: the majority has yet to secure any significant revenue, while still bleeding cash over product development and validation, with resulting negative profit rates in excess of two, sometimes three digits.

It is reassuring though to note that those with revenues exhibit a growing trend, reaching a total of 1B€ at end 2024 within Eurospace sample. With such levels of revenue coming on top of the fundraising activity, and despite the heavy cost of personnel associated to growing their capabilities, the largest and best funded European space start-ups have probably a few years of operations ahead of them.

And to conclude this short feature with a positive tone, there are a few companies in the Eurospace sample that are already posting profits. Interestingly they are not the largest or the best funded in the lot, but they obviously managed to navigate the development and validation route smartly to secure enough business to cover their costs in recent years. They are really worth a mention here: Open Cosmos (UK/Spain/Greece), Argotec (Italy), Officina Stellare (Italy), and Space Inventor (Denmark). There may be others, but we have yet to find them.

Pierre Lionnet is an economist with more than 30 years of experience in the space sector. He is a well-known expert of space markets and technology trends and the Research and Managing Director of Eurospace, the leading trade association of the European space industry.

[1] The Eurospace newspace observatory includes a watch-list of 1300 start-ups, mostly space pure players, having emerged in the past two decades. It focuses on upstream and midstream players, i.e; companies in the business of developing and deploying spacecraft and space launch systems. Pure players in the downstream are not on the list.

[2] This total includes the near 6B$ raised by Oneweb.

[3] I had a lot of thought considering Loft Orbital for the position, because they are developing fast their capabilities in France, but since their mothership is US-based it was hard to identify them as purely European.

Thanks for the recommendation. In Europe we focus especially on the field of space so much on the start ups. Sure, this is important but we should not forget to strengthen the already established (often medium seized) companies, which hold the market currently together. In my latest Substack post, I tried to comeup with an explanation why politicians currently love to talk about “innovation”: https://thetechnopolitical.substack.com/p/when-everyone-at-the-munich-security?r=30riyf&utm_medium=ios